Noam Galai/Getty Images Entertainment

Dear readers/followers,

In this article, I’m going to take another crack at what I believe to be a Tencent (OTCPK:TCEHY) proxy, namely Prosus (OTCPK:PROSY). I’ve been writing about Prosus owing to its Netherlands roots for over a year at this point, and my comments haven’t always been favorable.

However, I did establish a PT for the company – and the company hit this PT a few times last year. If you had followed that PT, which ranged from €40-€50 or so, with an average of €44-€45, you could have bought Prosus twice, and probably made some very decent returns if you look at today’s share price.

Seeking Alpha Prosus Article (Seeking Alpha)

Still, Tencent has done almost exactly the same journey, which is again why I call Prosus a “Tencent proxy”.

Tencent Share price (Seeking Alpha)

Still, let’s update on and see what we have going for us with Prosus here.

Prosus – Worth investing in here?

Oh, Prosus. I’ve been following this business for some time. It’s a tech investment company. A software disrupter that makes its money by investing in businesses in the relatively early stages of funding, and targets returns in the thousands of percentages. On a high level, the company has a lot of similarities with a venture capital firm.

It’s not a VC though – VCs and Angel investors tend to go in earlier than Prosus does, who focus on going into companies that, according to them, are already showing a fair bit of overall promise.

Prosus IR (Prosus IR)

The business idea is essentially to hold a portfolio of a lot of small companies, and hope that one of those companies really “pop”. That’s pretty much exactly what happened with Tencent. It is also what didn’t happen with about 20-50 other companies that Prosus has been investing in for years, and sometimes over 10 years. So it’s a high-risk high-reward profile where the theoretical quadruple or five-digit RoR makes up for what turns out to be sub-par investments that the company, in the best of scenarios can sell off at a small profit.

The risk/reward for a company like Prosus is absolutely core to its operations. Back in 2001, the company invested in relatively early funding in Tencent, buying nearly 45% (under 30% today) of the company for less than $35 million. For almost half of the company.

It was one of the most lucrative bets in corporate history, and it’s what Prosus has been riding since then.

Oh, you may say and argue that there are other great bets the company has – except no, not when you compare it to Tencent and nothing that’s actually showing the sort of promise we see in Tencent.

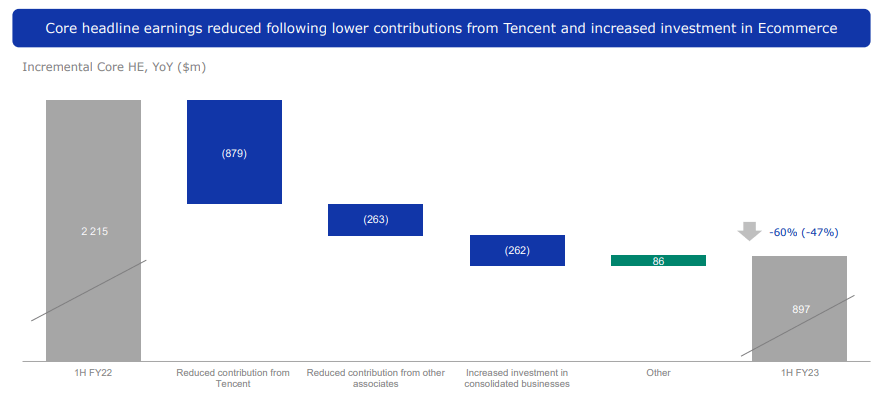

I am focusing on this investment a great deal because this is really quite significant for the company. Prosus’s net asset value, or assets overall, are still primarily made up of Tencent.

Since I first wrote about the company, its NAV has declined considerably. And it’s also still down more than 13%, which negates any and all recovery the company might have seen, in relation to that first stance, at least.

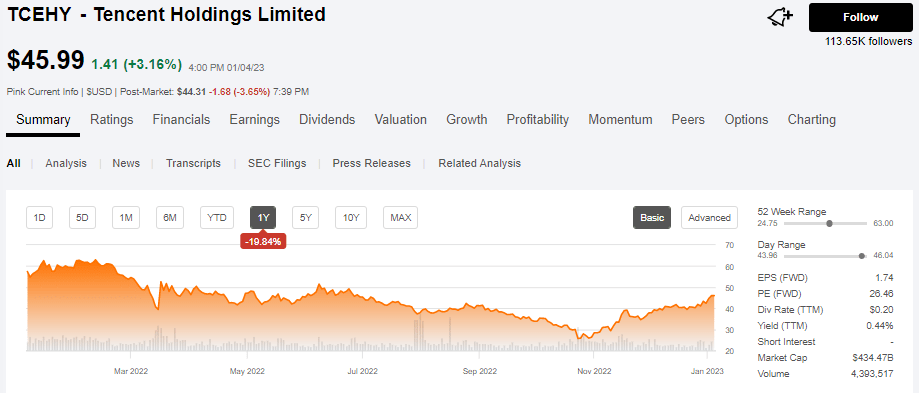

At the time the NAV for Prosus was around €130 per share. Today, that’s down to €108.8, with around €151B in asset value. Tencent remains around €120B of that, which means that no matter how Prosus spins and slices it up, it’s an 80% Tencent play – at least – and that’s a reduced Tencent stake from the last few quarters.

Aside from Tencent, the next largest holdings/investments are Deliver Hero and Trip – and it’s steeply downhill from there.

Prosus IR (Prosus IR)

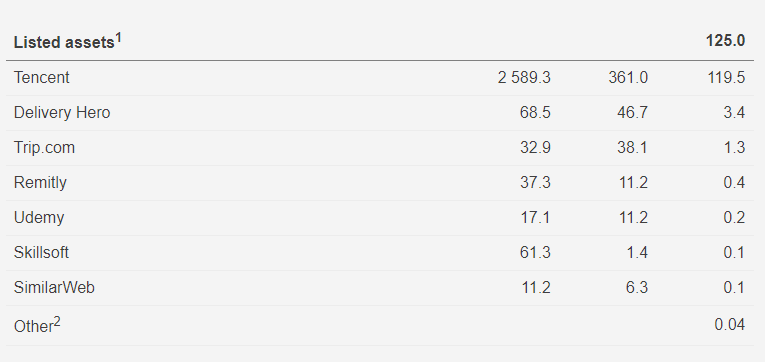

If you look at the company’s results, you’ll quickly notice a very clear trend. Prosus focuses on presenting revenue growth, order growth and transactions, courses or other measurables which make up what is essentially sales volume.

Prosus IR (Prosus IR)

That is because few of Prosus investments are actually successful businesses, in the sense that they do not make a profit yet. The company has deployed cash from income, and other things into buybacks and new investments. However, the buybacks in turn increase the company’s exposure to Tencent, which might not be what we’re looking for in an already 80% exposure to a volatile geography.

The Tencent drop also resulted in significantly lower contribution, in addition to FX, leading to the need for stringent and careful cost management. Again, revenues are up, but trading losses are exactly in the wrong direction. Take OLX group, for instance.

Prosus IR (Prosus IR)

Yeah, revenue is at record levels – but so is the trading loss/bottom line. This seems almost like a negative correlation – i.e. the more revenue the company makes, the less profit it actually generates- and that should be worrying to you as an investor. The exact same trend can be seen in Payments & Fintech, in Edtech (including Stackoverflow and Goodhabitz), leading to an increased focus on optimization and exiting underperforming businesses.

Prosus IR (Prosus IR)

In fact, the company gives us a target of consolidated profitability on an aggregate level for 1H25.

I’ve marked that date in my calendar and will be revisiting Prosus at that point to see if this was a target that the company can actually achieve. Because I do not believe that this business’s model allows for it – but I am more than happy to be proven wrong here.

Prosus is BBB-rated in terms of credit rating and has ~15000 employees working across most continents. The company is headquartered in Amsterdam, Switzerland, and listed on the Euronext stock market as a native share. So there is nothing fundamentally wrong with Prosus here.

Except how dependent it is on Tencent and how every step in the right direction (which it didn’t see at this time), is still not enough to offset an eventual Tencent decline.

Prosus IR (Prosus IR)

Now, some of my readers might say here that i “just don’t understand the way Prosus does business”. But I do understand – that’s exactly why I’m so hesitant about the stock, and why I’m asking/pleading with everyone who follows my writing to be careful as well. Despite Prosus being a BBB-rated business, this is not a risk-free or low-risk business. What else would you call a business that lost more than 50% of its share price in a single year?

Yes, it has low debt (based on LTV gross debt), good interest coverage, good cost of debt, and almost $15B held in cash at the central level. It doesn’t take away from that you’re investing much to get Tencent.

Now, if you want Tencent – then that’s a different story. However, the company still comes with issues, namely the way its relationship is structured with Naspers. Prosus itself is the international asset division of the South African parent company Naspers (OTCPK:NPSNY) (OTCPK:NAPRF). I go through this more extensively in my first article on Prosus, so the essentials are this.

Naspers controls Prosus – Prosus doesn’t and (likely) never, and you can never control Naspers. Even if Naspers’s actual stake were to drop to minuscule levels, they would still retain majority ownership over the company because of a clause that does not allow Naspers to fall below 50% voting rights.

This has been targeted by activist investors over and over again, and this sort of structure just leaves me with a bad taste in my mouth.

Because of all of these factors, I consider Prosus little more than a VC or Angel-investor alternative here. If you look at recent historical EBITDA levels, you will see that the company has shifted specifically to investing in food, edtech, and payment companies, but the increases in NAV in its legacy portfolio (including Tencent) have not been or barely been able to make up the losses initially suffered in these investments. Recent numbers do not reassure me even slightly, as losses seem to be increasing with revenue rising. This is not a strange or unexpected development given the increased cost of capital and the headwinds that seem to be coming to most tech-based businesses, but it does not make it better.

If you, as the investor, want to make the argument that Prosus’ previous investment in Tencent gives them some sort of success guarantee…well, be my guest – but that’s not how I see the market working.

Still, Prosus has solid fundamentals, and I don’t see any near-term risks given that the company can simply unload more Tencent shares if it needs the capital. It has cash, and it’s unlikely to run out of cash anytime soon.

The company “struck gold” with Tencent, but since then it’s been a line of relatively unimpressive overall deals – at best, some “good” deals that are offsetting what the company is pushing in terms of investing.

The company made a target in 2021, which I want to repeat here, namely that 2025 would bring $100B from e-commerce in NAV, which would rival Tencent. You’ll notice we’re now around 23 months from that particular point, and the respective NAV is about a third of that.

So, do you think that the next 23 months will be conducive to E-commerce as a sector in a way that will make it grow 2-3x? Because I don’t.

So, let’s see what happens – but I will continue to say what I’ve said before and what I’ve focused on – “Show me the money”.

And right now, the only company that really has done so is Tencent – and if I wanted Tencent, I could buy Tencent – and get a yield from the ADR as well as similar levels of exposure and trends.

Prosus Valuation

As I said in my first article, Prosus valuation essentially comes down to a single question. How much do you want to discount Tencent and the company’s NAV?

I invest in a lot of investment companies because Sweden has a tradition of having them. So this is not new territory for me. I’m quite familiar with investing in a business when the NAV/share of that business according to me, is favorable in terms of the value that’s being offered – i.e when it’s undervalued.

Because of that, I view Prosus as fairly easy to value, because I know what I believe it to be worth, i.e. how much I would discount the NAV of the company. When I invest in investment conglomerates (and I do, over 6% of my portfolio is allocated to several of them), I do so on the basis of NAV taking center stage here.

1:1 NAV is a guidance mark – and where I would be accepting things if the company had a solid set of dividend-paying companies added to by some nice investments that are not public, but also pay a nice dividend.

That is not the case here with Prosus – Prosus, as I see it, cannot justify a 1:1 NAV/share price target.

All of my investment holdings have 90%+ listed portfolios of quality companies often going back 100+ years. They pay a yield. They’re not flighty or sudden with their allocation or investments. They have very specific strategies for holdings and holding times (usually forever) that I agree with.

Prosus, on the other hand, is closer to a VC/Angel company that tends to buy, then divest the company when its IRR is met (see the sale of Avito). They are not long-term holders, and I am often left in the dark as to their decisions and logic, which means I’d have to trust them to do this effectively. That requires discounting.

Discounting isn’t a problem. There isn’t one company I don’t discount in some way. I present you with the following questions that you could ask to see how far you’d want to discount Prosus before investing:

- How much do you want to/should you discount the company’s NAV/share in terms of risk/reward for its strategy?

- How much should you discount the company’s NAV/share to reflect its stake in Tencent, given the geopolitical risks of China and the current market situation, and how the share has performed in 2022?

- How much premium or discount do you believe should be applied for management capabilities or expertise, given historical performance?

- What should the discount be for the company’s shareholder relationship with Naspers, which means that Prosus is never really in charge?

It’s currently at a NAV/share of €108, with a share price of €72, implying a decent discount – but not an interesting one, as I see it.

Because Prosus is 80% Tencent, a risky china-based investment, I would discount it by 70% before going in. Due to the lower NAV, that means I’m lowering my PT for Prosus to below €40/share, to a €35/share. I’m allowing for the NAV to climb back up slightly.

Keep in mind, Prosus has actually underperformed most broader indices. When I first wrote about the company, it had barely managed to keep up with a 2-year return of 20%, and that was during the tech froth.

The one avenue of entry I see with Prosus is treating it like a somewhat enhanced way into Tencent. If you can buy it at €35-€40, then your potential rebound performance is significant/can be significant – as you’ve seen when you look at my latest article to this one.

But the combination of higher interest rates, the risks to the company’s business model, and the current trends which show development in only one direction, dictates that I as a valuation investor approach Prosus with great care.

And currently, this means saying “no”.

Keep in mind, I don’t consider it “wrong” as such to discount Prosus to a lower degree than I do – but I would caution you. My discounting comes from some experience with risky investments such as these.

If you discount it less, you should have a reason for it.

This is my current Prosus thesis going into 2023.

Thesis

My thesis on Prosus is as follows:

- Prosus is an investment that’s inherently different from buys I would consider due to its almost Venture Capital-like approach to investments and targets.

- The shareholder structure is unappealing and inherently disadvantageous to Prosus investors. While the company is fundamentally sound and has a good track record due to the Tencent investment, there are too many fundamental question marks to really make this an option for me.

- I would be interested in Prosus if the market decided to discount it more than 70% to its current NAV. That currently comes to below €40/share but would change depending on the impact of Tencent.

- If Tencent drops, the company’s NAV drops with it – and quickly. A 50% drop in Tencent’s NAV would drop the company’s NAV by around 38%, showcasing just how tightly the company is tied to Tencent. We’ve seen this over the past half-year, and even with recovery now, it’s only adding to the volatility

- I consider it a “HOLD” here. My PT is €35/share.

Remember, I’m all about

1. Buying undervalued companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime. Even if that undervaluation is slight and not mind-numbingly massive.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn’t go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

Too few of my criteria are fulfilled by the company. I can’t call this anything except a “HOLD”.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

{kind=link}