Stay informed with free updates

Simply sign up to the Residential property myFT Digest — delivered directly to your inbox.

One of the most powerful cultural myths of the English-speaking world over the past century has been the belief that if you work hard, you’ll earn enough to buy yourself a house and start a family.

For a long time, it held true. Between the end of the first world war and the turn of the millennium, rates of home ownership climbed rapidly in both Britain and the US, topping out at about 70 per cent as young adults flew the parental nest and set up homes of their own.

But in recent decades, that trend has not only stalled but reversed. In 1980, almost half of 18 to 34-year-olds in Britain and America lived in their own property with children of their own, making this the most common arrangement for young adults. Today that is true of only about one in five, and the most common set-up for 18 to 34-year-olds is now to be living with their parents.

While some of this is due to the expansion of higher education, the trends hold true even after excluding students. The dream of a family home of one’s own has become just that — a distant dream.

But while the housing affordability crisis gets a fair amount of airtime, it often feels secondary to other leading concerns of the day. The breakdown of a central aspirational belief across the wider Anglosphere is at risk of becoming background noise.

One key reason for the lack of serious attention or action is age, which works in two ways. First, the people most acutely affected by this problem are from an age bracket that still exercises little political clout by voting. Second, few above the age of about 45 — ie virtually all key decision makers — appreciate what it’s like to have this particular key rite of passage postponed, sometimes indefinitely.

The latter point is under-appreciated. We have long-established ways of both discussing and tackling recurring economic shocks such as recessions or inflation. Every tool in the box is thrown at the problem, and the media, politicians and the public alike talk of little else until the worst is over. But the housing crisis is different. There are no recent playbooks to draw from.

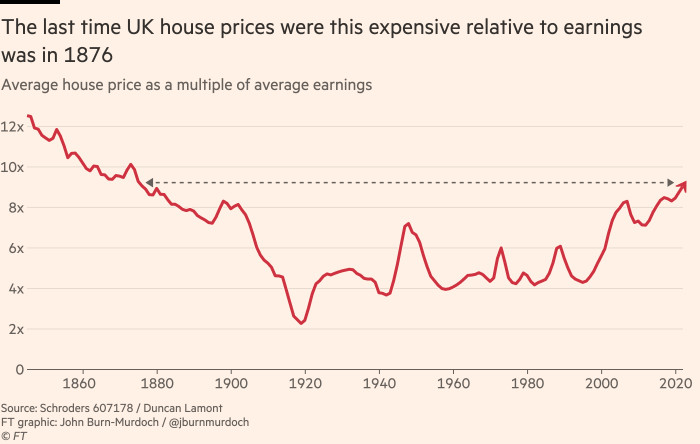

Aside from the occasional blip, average house prices were roughly four times average earnings in the UK for 80 years between the 1910s and 1990s. This was a fixed characteristic of British society. Knuckle down, save for a few years and buy in your late twenties: simple. Then the ratio doubled in the space of a decade. The last time it was that high, cars had not yet been invented, Queen Victoria was on the throne and home ownership was the preserve of a wealthy minority.

To put the price-to-earnings ratio into more tangible terms, it now takes 13 years to save a deposit for the average UK property (up from three in the mid 1990s), and 30 years in London (up from four). To state the obvious, nobody spends 30 years saving for a house. The dream is over.

But despite such a historic economic and societal shock, the response from politicians and policymakers has been muted, in sharp contrast to the recent inflation spike.

Economists, central bankers and politicians spent the past two years battling a cost of living crisis that saw prices rise by an estimated 20 per cent in total, largely offset by pay increases. Whereas a 100 per cent real-terms increase in the unaffordability of perhaps the single most important good in modern western society has generally been treated as a young person’s issue with politicians paying only lip service to solutions.

The breakdown of the housing conveyor belt has huge and diverse impacts. Studies show that the inability to afford a home causes people to postpone starting a family or simply not have children at all. High housing costs also divert individuals away from productive places and activities, and dramatically increase inequality in wealth and between regions.

With big elections on the horizon on both sides of the Atlantic, politicians are relieved that they can point to encouraging signs about inflation’s possible return to normal levels. The housing affordability crisis shows no signs of following suit. It should be at the top of the agenda as the political campaigns get under way.

{kind=link}